Throughout the past three years, Egypt initiated a series of tough, yet essential economic reforms, undertaken by the authorities and supported by the International Monetary Fund (IMF).

The economic reform programme aims to transform the country’s economy through improving public finances, curbing the budget deficit, and getting the currency shortage under control, all while achieving sustainable growth.

The Egyptian economy has started to recover, with GDP growth improving, foreign reserves reaching their highest level on record. This renders 2018 a potential turning point for the country, following years marked by turbulence and uncertainty, accompanied by numerous challenges that faced the Egyptian economy, from political unrest and declining tourism, to foreign currency and fuel shortages.

The country’s economic momentum has eased, but Egypt’s fundamental recovery story remains intact, according to the Middle East Overview Outlook 2019 report issued by the Switzerland-based investment bank, and financial services company, Credit Suisse Group.

Credit Suisse maintained a positive economic outlook for the Egyptian economy, yet they highlighted some challenges such as reliance of reserves on hot money flows, weak foreign direct investments (FDI), elevated headline inflation, and policy uncertainty rising from unexpected tax amendments.

“We continue to see the recovery in tourism and transition to being a net gas exporter driving growth and underpinning currency stability into 2019,” the report states.

Adding that from their vantage point, Egypt’s equity market sell-off is overdone, but with technicals – analysis employed to evaluate investments and identify trading opportunities by analysing statistical trends gathered from trading activity, such as price movement and volume – still looking weak a near term recovery looks difficult.

Economic momentum, growth slowing, long-term recovery remains intact

Economic momentum, growth slowing, long-term recovery remains intact

According to the report, the Purchasing Managers’ Index (PMI), which measures the performance of manufacturing and service sectors, dropped to an 11-month low on slowing economic momentum. After being above 50 (expansion) for two consecutive months – the first time since September 2015.

Consequently, this is also reflected in industrial production growth, which has fallen from its Q3 of 2017 peak.

However, Credit Suisse believes that Egypt’s growth levels are still far from being contractionary, and there are early signs of stabilisation.

The report indicated that, taking into consideration the scale of structural reform required in Egypt, a recovery was never going to be in a straight line, and that the investment bank remains positive and confident of the long-term recovery trend.

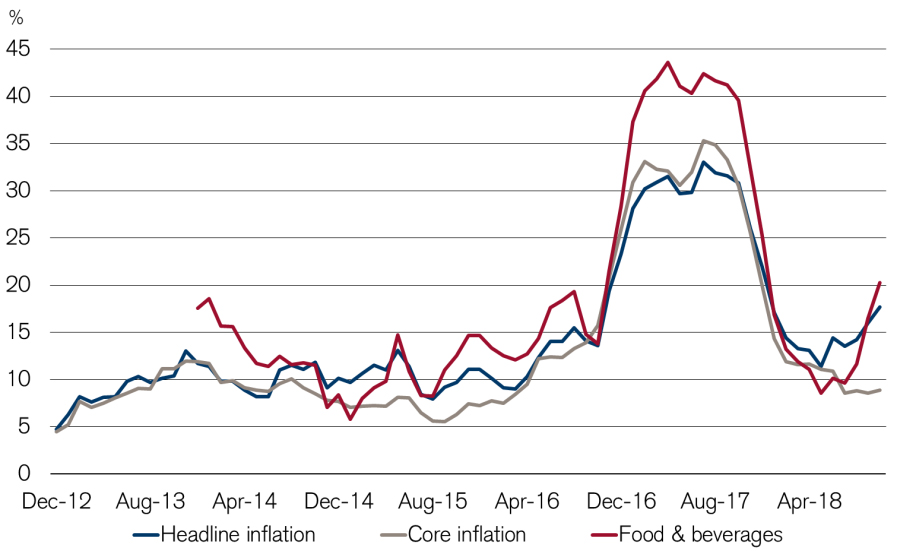

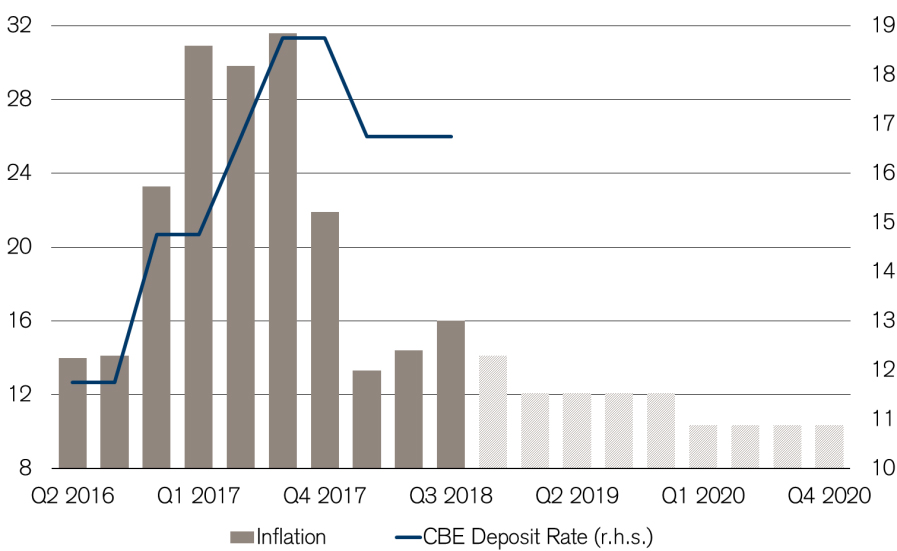

Inflation elevated, still within CBE’s target

Headline inflation shot higher to 17.7% in October 2018, primarily on food inflation but also due to planned adjustments in regulated prices, before dropping to 15.7% in November, yet it still above the CBE’s outlook of 13% (±3%) in Q4 of 2018.

However, the report indicate that such rates are not a significant issue, especially since core inflation has continued its decline to the lowest level in almost three years.

In a measure to control inflation, the CBE hiked interest rates by 700 bps since the 2016 devaluation, and the report forecast further rate cuts. However, elevated oil prices, investor risk aversion toward emerging markets (EMs) and high headline inflation will likely prevent any such cuts near-term and we look for a further rate cut in Q1 of 2019 at the earliest.

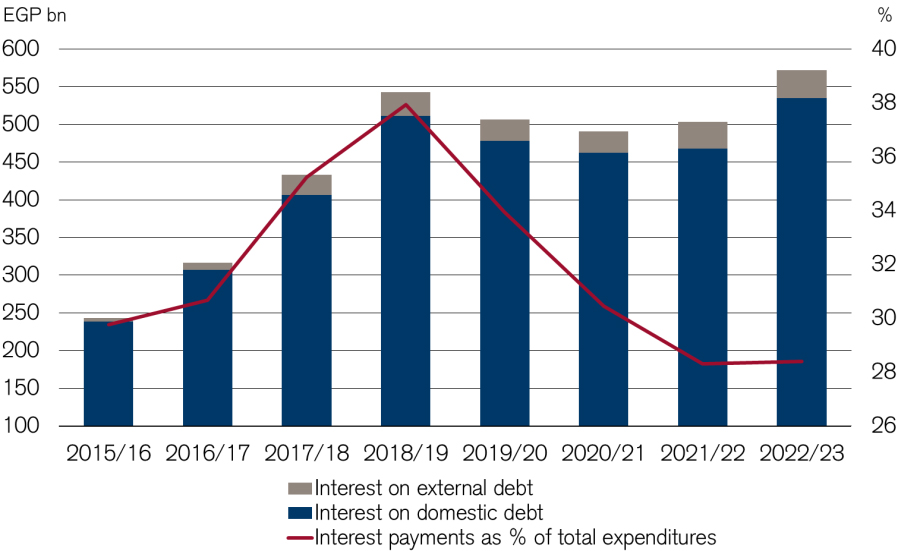

Fiscal deficit, debt profile on a recovery path

According to the report, Egypt recorded its first primary surplus in 15 years for 2017/18, and the bank forecast it is on track for its targeted 2% primary surplus next fiscal year (FY).

These positive developments were also reflected by Moody’s action to upgrade Egypt’s sovereign rating outlook to positive (from stable) in end-August, due to its business sector reforms and continued improvements in its fiscal and current account balances.

The report indicates that, although debt levels are elevated overall, they are projected to decline consistently over the coming years on fiscal consolidation. Repayments are expected to ease after peaking this FY.

LNG imports halt, improving current account position

LNG imports halt, improving current account position

With production at the Zohr gas field ahead of schedule, Egypt officially stopped being a net LNG importer this month. Daily gas output fell from 7bn cubic feet per day (bcf) in 2010 to 4 bcf in 2016 but rose for the first

time in several years to 4.5 bcf in 2017.

The report indicated that over the next three years, production is projected to increase to 7.7 bcf, well above Egypt’s domestic needs of 5.2 bcf. On-going exploration activities have the potential to further boost Egypt’s production capacity.

Consequently, strong improvement in Egypt’s current account balance are expected, thus it is one of the key factors behind the investment bank’s expectations of the EGP’s stability into 2019.

Exports, tourism, remittances, leading the way to recovery

Egyptian exports have clearly started to recover, driven by the removal of currency-related uncertainty, the report states.

Furthermore, looking at the long-term history in both dollar terms and as a share of the GDP, it is clear that there is considerable scope for further recovery over a multiyear period.

Credit Suisse believes that the export industry is a critical part of the economy, and is also a key source of hard currency, hence its recovery will be important to monitor.

On the tourism front, the report indicates that revenues show impressive strength, affirming its position as an important source of both forex and labour employment.

The sector is firmly in recovery, with tourism revenues approaching previous peak levels despite the number of tourists still well below the 2011 peak – which the report believes is due to a change in the mix of tourists and the EGP depreciation. The recovery and sustainability of these flows is absolutely key.

However, the investment bank believes, that Russia’s decision to reinstate flights to Cairo after a break of almost 2.5 years is positive, as restoring flights to Egypt’s resort cities of Sharm El-Sheikh and Hurghada, would further boost tourism arrivals, especially since it could prompt the UK to resume its own flights as well. Both Russia and the UK are among Egypt’s most important sources of tourists.

In regard to remittances, a surprising increase in remittances has led to sharp upward revisions in the IMF’s projections and has also provided support to Egypt’s current account balance.

However, according to the report, this is unlikely to be sustainable since it has been driven in part by expats leaving Saudi Arabia in the wake of its Saudisation efforts. The level at which remittances will stabilise at is critical.

Moreover, the report highlights, slow foreign direct investments (FDI) is the primary area of disappointment in Egypt’s economic development. Not only it has significantly lagged expectations, but the momentum has slowed,

with the 12-month moving average having peaked in end-2016.

External balances showing strong improvement, all time high reserves support currency

External balances showing strong improvement, all time high reserves support currency

Reserves continue to reach new all-time highs, backed by the IMF programme, successful bond issuances, and an ongoing recovery in tourism.

“We remain concerned over the reliance on ‘hot money’ flows, but we see reserves as being sufficient to keep from another EGP devaluation,” said the report.

The report indicates that taking into consideration, the CBE recent decision to end the repatriation mechanism, fluctuation around EGP 18 can be expected, as all flows will now go through the interbank market.

However, the investment bank forecast that the government will want to avoid sharp weakness in the EGP as this could attract speculative pressures and may risk social unrest.

Consequently, the report expects just a modest EGP weakness, despite the sustained dollar strength and risk aversion against EMs.

T-bills continue to offer compelling returns, despite decline

Foreign holdings of Egyptian treasury bills (T-Bills) have declined significantly in recent months, although they

remain just above peak-2010 levels. Moody’s upgraded Egypt’s outlook to Positive from Stable in August 2018.

As a result, Credit Suisse continue to hold a positive view on T-bills, which they believe are oversold, noting that yields appear to be rolling over.

“We see limited downside risk to returns from EGP weakness. The cancellation of long-term T-bond auctions in September was worrying, but we believe it was a function of EM trade tensions and not Egypt’s fundamentals. Indeed, we believe it points to encouraging discipline from the Egyptian government,” the report added.

Credit Suisse maintains positive view on equities, despite recent sell-off

The report cites, the recent sell-off in Egypt and EM equities coupled with continued growth in Egyptian earnings expectations has pushed Egypt’s price to an earnings ratio (P/E) which is at a 3-year low.

However, the investment bank maintains their positive view on Egypt, and sees the recent sell-off as an opportunity to add exposure. Taking into consideration the recovery in earnings forecasts since the devaluation, although in dollar terms, the economy has just now returned to pre-devaluation levels.

The report indicated that it is important to keep in mind that over the past two years, earning per share forecasts have increased 42% in Egypt in USD terms (65% in nominal EGP) compared to 14% for the Middle East and 28% for Morgan Stanley Capital International (MSCI) EMs.